![]()

![]()

The Alcohol and Tobacco Levy Act of 2019, which provides for the imposition and collection of a levy on alcoholic beverages and tobacco products and other incidental matters.

1st October 2019. Imports made from this date will be subject to the levy, as well as local sales made by manufacturers.

(NB: Local retailers are NOT expected to collect the levy)

Local manufacturers of alcoholic beverages and tobacco products are expected to submit ATL Returns. All returns and payments are due by the 20th of the following month.

YES, the taxpayer is expected to submit a NIL ATL return.

No. ATL is non-refundable nor deductible as input tax.

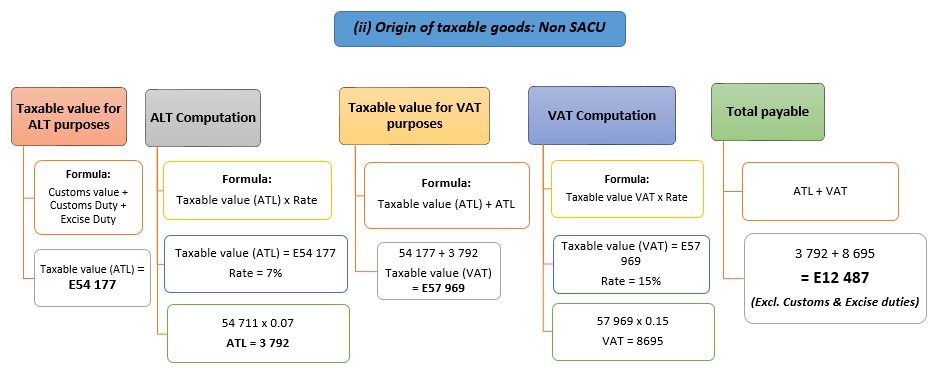

The taxable value for ATL purposes is critical in the computation of the correct amount of ATL payable to the ERS. The working out of the taxable value is illustrated in the examples below:

(Click on the images to enlarge viewing)

Note:

With effect from 1st August, 2018 the VAT rate will change from 14% to 15%.

Businesses that are making a taxable turnover of E500, 000 or more per annum.

Registration is not mandatory if the taxable turnover is less than E500, 000/annum, but a business may register voluntarily if they comply with the requirements for registration as stated in the VAT Act. E.g. does the business have a fixed place of doing business in Eswatini; is the business able to keep proper books of account; will the business be able to submit accurate returns as and when required by the Act.

The import VAT relief on goods worth up to E1,000 (one thousand Emalangeni) is provided on the following conditions:

* It is ONLY for bone fide personal imports; any goods that do not fit this description will not qualify for the relief.

* You must have been out of Eswatini for a minimum of 48 hours.

* You must not have elected to declare the goods using the Sekulula VAT Easy system.

A. Non -Profit Cultural and Amateur sporting activities

B. International Agreements

C. Diplomats, Diplomatic and Consular Missions

A. Amateur (unprofessional) organization of sporting activities and non- profit and cultural activities and services.

B. International Agreements

C. Diplomats, Diplomatic and Consular Missions and international organizations

The deadline for VAT online filers is the 27th of the following month after the end of the tax period. They must be submitted on E-Tax

View all Application Forms

View all Customs and Excise Forms

View all VAT Forms

View all Income Tax Forms

View all Other Forms

Provisional Tax:

1st payment is due no later than 31st December

2nd payment is due no later than 30th June

3rd payment is due on receipt of Notice of Assessment after having submitted Income Tax returns

Remittance of PAYE:

No later than the 7th every month

Publications

Payments

© 2024 Eswatini Revenue Service. All rights reserved

Website Designed by Real Image Internet